Read Time:

5-minute

article

Help your children get the most of their first post-college job

This content is categorized as:

If your child has recently graduated from college and is starting a first job, it can be an exciting and nerve-wracking transition. College probably did a great job preparing your graduate for the technical aspects of a new career. But there are softer skills your child may not be thinking about like accepting feedback from a leader, networking with peers or taking best advantage of employee benefits.

Not all adult children may welcome advice from their parents, but if your kids are open to your guidance, here are a few new job tips to share:

Learn your manager’s style

Forming a good relationship with your leader can be essential to getting the most out of your first job. Find out your manager’s preferences and expectations, provide frequent updates on your projects, ask for occasional feedback if your leader doesn’t provide it and respond positively to constructive criticism.

Be professional

In college, you may have been used to sliding into class a few minutes late or dressing casually every day. But once you enter the work world, a professional approach can go a long way toward success in your new job. Pay attention to your office’s culture and follow your manager’s and coworkers’ lead regarding start and end times, lunch breaks, your wardrobe and overall appearance. Be mindful not to overuse your personal cell phone — and if you feel compelled to check social media or text a friend, try to do so privately on a break and away from your workspace.

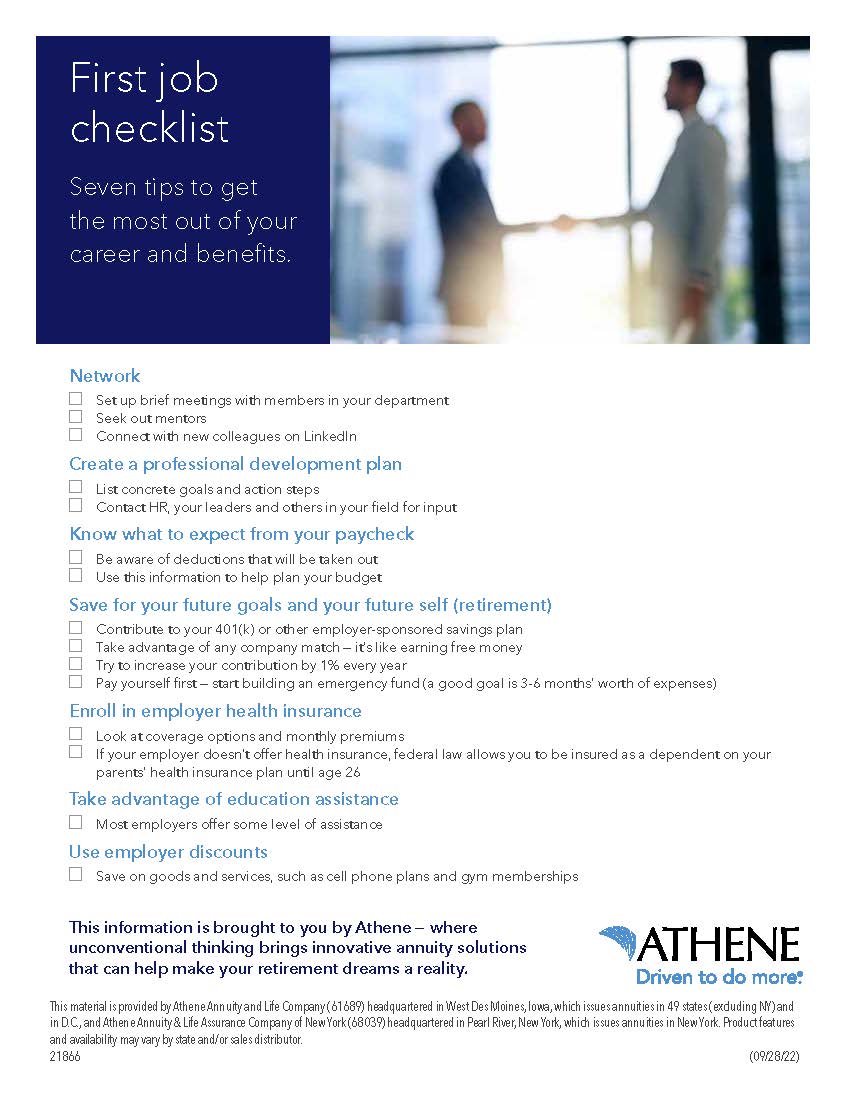

Network

Set up brief meetings with each member of your department to find out what their role is, what they’re working on, how you might be able to help them and what they’re interested in outside of work. Also seek out mentors or sponsors — people with more experience who can help guide you toward success. If there are employee resource groups in your company, they can be a great place to network and find colleagues interested in helping you develop your career.

Create a professional development plan

To help advance your career, it’s important to create a strategy that includes concrete goals and action steps. Many companies will provide you with a development plan framework, but if yours doesn’t, create your own plan. Talk to Human Resources, your leader and others in your field to find out what certifications, courses, degrees or professional groups might help with career advancement.

|

Need a little extra help guiding the conversation?

Here’s a useful checklist to help them stay on track.

Download now

|

Make the most of your company’s benefits and compensation package

(Parents, here’s an area where your guidance can be invaluable, especially if you’ve footed the bill in the past and your kids haven’t had to think much about finances.) Here are a few key tips to keep in mind when starting your first post-college job:

Know what to expect from your paycheck

If you haven’t started your new job yet, be aware of the deductions that will be taken from your paycheck. Deductions will include federal income tax, federal and state insurance taxes, Medicare taxes, state income taxes and any contributions you elect, like your 401(k) and benefits such as health insurance or disability insurance. If you want to know approximately how much your first paycheck will be, here’s a helpful Paycheck Calculator.

Save for your future goals and your future self (retirement) — contribute to your 401(k) or other employer-sponsored savings plan

A specific percentage of your salary will be automatically withheld from your paycheck using pre-tax dollars. To help people save for retirement, many employers also contribute to their employees’ 401(k). A typical employer match is 50 percent of what an employee contributes, up to 6 percent of the employee’s salary, but some employers may match more. Be sure to take advantage of this free money! You’ll see the power of compound interest work as your 401(k) grows tax deferred until you withdraw it in retirement.

When you may still be paying off student loans and have other expenses to think about, it can be hard to prioritize saving for retirement. But start saving now while time is on your side. For example, at age 22, if you earned a salary of $50,000 with 3 percent wage increases each year through age 65, and you contributed 6 percent to a retirement account and your employer matched 3 percent, you could retire with more than a million dollars at age 65. But if you wait until the age of 35 to start saving, assuming a salary of $50,000 at that age, your retirement savings could be less than half the amount. To figure how much you should save, try a 401(k) calculator.

Enroll in employer health insurance

If your employer doesn’t offer health insurance, federal law allows you to be insured as a dependent on your parents’ health insurance plan until age 26. If your employer does offer health insurance, they’ll usually pay a percentage of the monthly premium. Employers in the private industry pay an average of 79 percent of the monthly premium for single coverage, and deduct the rest from your paycheck.

If your employer offers multiple health insurance options, weigh the various plans and these considerations:

- What services are covered (especially important if you have a health condition)?

- What providers are covered?

- If you take prescriptions, are they covered and what’s your share of the cost?

- How much will it cost, considering both your monthly contribution toward your premium, as well as any deductible and copayment amounts you pay out-of-pocket toward your care?

Take advantage of education assistance

Nearly 80 percent, of employers offer opportunities to develop new skills and 48 percent provide undergraduate or graduate assistance as a benefit. Some employers are even helping employees pay back their existing student loans.

Use employee discounts

Many employers offer discounts toward things like cell phone plans, gym memberships, tickets to local sporting events or company products.

Want the most from your retirement? Get smarter with Smart Strategies from Athene. Your source for tips, tools and financial solutions that can help you live your best life.