Read Time:

6-minute

article

5 reasons to consider a custom index within your FIA

This content is categorized as:

Fixed indexed annuities (FIAs) are in high demand. For people building retirement savings, FIAs are a popular choice because they can help address threats to your retirement strategy such as market uncertainty, outliving your savings or inflation.

Why choosing a custom index is an important part of your FIA

Fixed indexed annuities are one way to potentially increase your retirement savings without risking loss due to market downturns.

If you’re using your FIA to help increase retirement savings, you’ll earn interest credits based in part on the performance of a benchmark index. You’ll select crediting methods and indices, and you may be able to choose a custom index. Here are a few reasons you may want to take a closer look at these options.

Unique ways custom indices drive value in a FIA

1. Custom indices are designed specifically for FIAs.

Benchmark indices are typically offered within a FIA but were created before FIAs were developed and may not match the goals of today’s retirees. In contrast, custom index options were developed specifically for FIAs. They are created using advanced technology, predefined rules and automatic tracking to monitor their effectiveness and performance. Unlike an actively managed index, custom indices have preset criteria and can react far more quickly to changes in the market or set criteria. Custom indices are developed by reputable index houses, large investment banks and asset managers according to stringent protocols. As a growing field, increased availability helps ensure competitive pricing and features that benefit customers.

2. Built-in diversification helps improve the balance between risk and reward.

Diversification is commonly explained as “not putting all your eggs in one basket.” By spreading out allocation options, risk can be reduced and the potential for higher returns may increase. Custom indices offer the possibility of diversification beyond the U.S. large-cap equities included in the S&P 500®. They can be based on U.S. equities only, global equities, equities and bonds, or multiple asset classes, that is, equities, bonds and commodities. Because the custom index is inside of a FIA, there is added protection from market loss. In addition, allocations can move from one asset class to another depending on how the custom index was created and how the market is performing. This helps take some of the guesswork out of managing your allocations inside of the annuity.

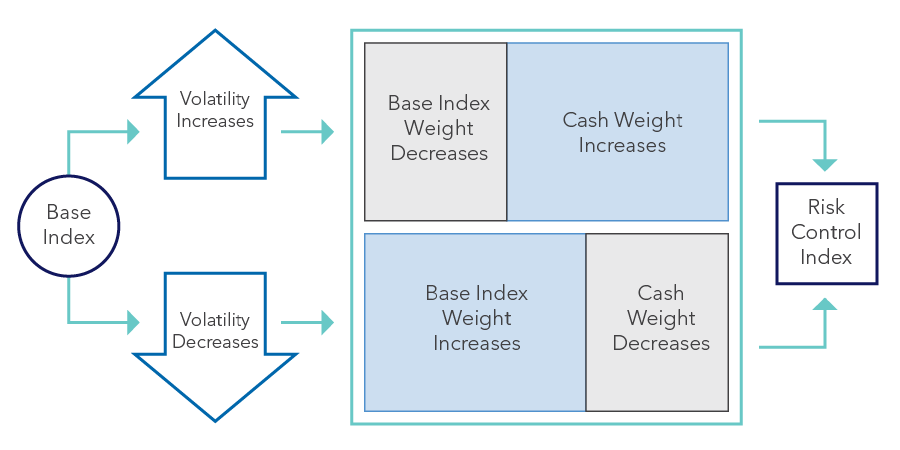

3. Volatility control feature helps ensure “a smoother ride.”

A custom index has a volatility control feature which acts like a car’s shock absorber to cushion passengers from bumps in the road. The volatility control feature tracks index volatility (the “bumps in the road”), and as bumpiness increases, the feature seeks to cushion returns by decreasing exposure to the risky asset(s) and increasing exposure to a stable asset, like cash. The volatility control feature is designed to maintain the volatility of the index at a preset “target” level, such as 5%. For comparison, the long-term volatility of the S&P 500® index is around 15%.

4. Higher participation rates mean higher growth potential.

In a FIA, a participation rate can determine the potential interest credit you’ll receive. It can be used either by itself, or along with a cap or other features. It acts as a multiplier on an increase on the index, if any. For example, if the index increased 50 percent, and the participation rate was 130 percent, the index would credit 65 percent. (50 percent x 130 percent = 65 percent.) Because custom indices are created specifically for FIAs, they have specific efficiencies and cost effectiveness built into their design. In addition, the volatility control feature allows for more predictable performance making it possible for the insurance carrier to offer higher participation rates.

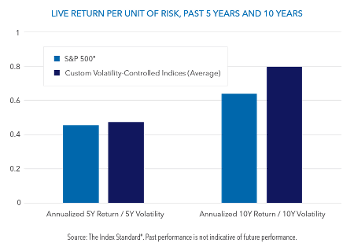

5. “Apples to apples” comparisons favor custom indices.

When making an “apples-to-apples” comparison among custom indices and benchmark options, the measure used is a ratio of average index return to average index volatility. Research from The Index Standard® compared the performance of long-standing custom indices used in FIAs to the S&P 500® Index, based on 5 and 10-year live periods.1 Using this simple measure of efficiency, custom indices on average outperformed the benchmark in both cases.

Custom indices can be a valuable part of a holistic strategy and can increase the potential for positive outcomes inside of a FIA. They also offer downside protection in volatile markets, with volatility control features that help enable higher and more stable participation in positive markets.

Ultimately, choosing to use a custom index will be based on your personal goals, concerns and comfort level. Talk with your financial professional to be sure you understand how a custom index in your FIA may benefit your situation.

Want the most from your retirement? Get smarter with Smart Strategies from Athene. Your source for tips, tools and financial solutions that can help you live your best life.

1 The Index Standard® filtered custom indices currently used in FIAs according to the length of their live performance record (i.e., the time since their launch): indices with at least 5 years of live performance (a total of 67 indices); and indices with at least 10 years of live performance (a total of 15 indices). For the two sets, the average annualized index return divided by the average annualized index volatility was computed for each index over the 5 years and 10 years ending June 30, 2022, respectively. The same ratio was computed for the S&P 500® price return index (ticker SPX) for the two periods. The chart shows the average value of this ratio for the custom indices compared to this ratio for the S&P 500® for each of the two time periods.

The "S&P 500®" is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and has been licensed for use by Athene Annuity and Life Company. Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Athene Annuity and Life Company. Athene Annuity and Life Company’s products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500®.

Indexed annuities are not stock market investments and do not directly participate in any stock or equity investments. Market indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an index nor any market-indexed annuity is comparable to a direct investment in the equity markets.