Read Time:

4-minute

article

What can RILAs and VAs do for you?

This content is categorized as:

Both registered index-linked annuities (RILAs) and variable annuities (VAs) can offer viable options for your retirement income strategy; however, there are important differences to understand.

What is the difference between a VA and a RILA?

VAs enable investors to directly participate in an investment option (like mutual funds), while a RILA credits interest based in part on the upward movement of a market index, like the S&P 500®.1 A RILA is sometimes described as a cross between a fixed index annuity (FIA) and a variable annuity, as it offers less downside protection than a FIA but accepts a level of market risk in exchange for higher growth potential.

Why are annuities often misunderstood?

Despite their longevity, annuities are often misunderstood. Why the stigma? There are a few possible reasons. Annuities are sometimes seen as complicated as there are many different types. Others may view them as risky or only for the very wealthy. But when you evaluate your retirement needs and goals and get a basic understanding of annuities, it’s easier to get a clearer picture of how annuities might fit into your retirement strategy. For now, let’s take a look at the solutions RILAs and VAs can provide.

What are some common types of annuities?

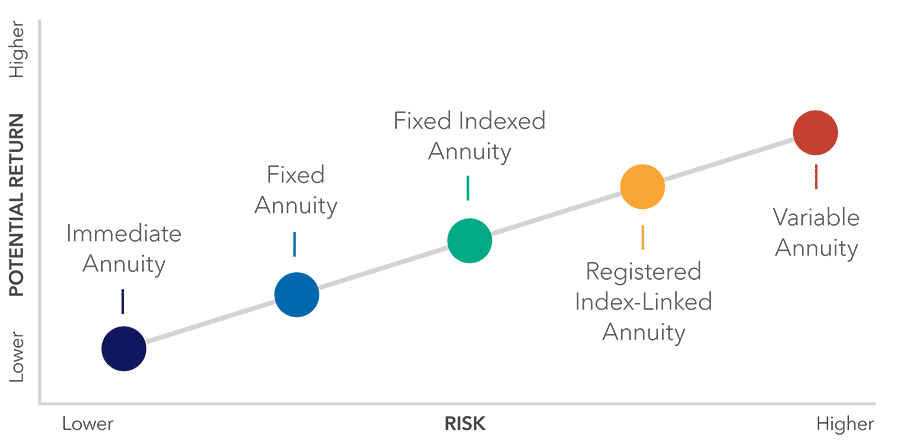

VAs, immediate annuities, RILAs, and FIAs are some common types of annuities. They are each designed for different needs and risk tolerances.

Like any financial product, annuities are right for certain circumstances, but may not be appropriate for all situations. As mentioned before, there are several types of annuities to help fit different needs. Most people buy an annuity to help with long-term financial goals like generating guaranteed lifetime income, accumulating money for retirement or helping to protect savings from market loss.

An important note is that all annuities are insurance contracts. In exchange for following the rules of the contract, a person will receive certain guarantees that are backed by the financial stability of the insurance company.

Another way annuities vary is by the amount of potential risk and return.

How does a VA work?

Variable annuities allow for direct participation in a number of investment options, including mutual funds. The money you allocate to each investment option will increase or decrease depending on the fund's performance. While VAs offer higher growth potential, they also have higher risk than other annuities. People often buy VAs for their growth potential as well as for features that can help turn that growth into income during retirement.

What are the pros and cons of a RILA?

RILAs are a newer type of annuity. People generally buy RILAs for growth potential, as they offer the opportunity to earn interest credits based in part on movement of a stock market index. Unlike a variable annuity, RILAs have features that provide a measure of protection in case of market loss. However, a higher level of protection from downside risk means a lower cap on upside potential, and vice versa.

From a risk standpoint, a RILA can be described as a cross between a FIA and a VA. A RILA may be a good match for you if you want a level of downside protection but are willing to accept some market risk. It’s important to know your annuity “comfort zone” when it comes to your tolerance for risk.

Discuss your retirement goals with your financial professional to help determine if annuities are the right fit for you as part of a holistic retirement strategy portfolio.

Want the most from your retirement? Get smarter with Smart Strategies from Athene. Your source for tips, tools and financial solutions that can help you live your best life.

1 The S&P 500® Index (the “Index”) is a product of S&P Dow Jones Indices LLC or its affiliates (“S&P DJI”) and has been licensed for use by Athene Annuity and Life Company (“Athene”). S&P®, S&P 500®, US 500, The 500, iBoxx®, iTraxx® and CDX® are trademarks of S&P Global, Inc. or its affiliates (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Athene’s products are not sponsored, endorsed, sold or promoted by S&P DJI, Dow Jones, S&P, or their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the Index.

Registered index-linked annuities have a risk of substantial loss of principal and related earnings. They are designed to be a long-term investment product used to help provide income for retirement and are not suitable as a short-term investment. Registered index-linked annuities can only be marketed and sold by securities licensed financial professionals. Any discussion of this product must be preceded or accompanied by the product brochure and prospectus which provides more detailed product information, including all charges or limitations as well as definitions of capitalized terms.

Indexed annuities are not stock market investments and do not directly participate in any stock or equity investments. Market indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an index nor any market-indexed annuity is comparable to a direct investment in the equity markets.

**Withdrawals and surrender may be subject to federal and state income tax and, except under certain circumstances, will be subject to an IRS penalty if taken prior to age 59½.

Guarantees provided by annuities are subject to the financial strength and claims-paying ability of the issuing insurance company.

Guaranteed lifetime income is available through annuitization or an income rider. Income riders may be built into the contract or optional for a charge.

Indexed annuities are not stock market investments and do not directly participate in any stock or equity investments. Market indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an Index nor any market-indexed annuity is comparable to a direct investment in the equity markets.