Read Time:

5-minute

article

Recalibrating risk tolerance

This content is categorized as:

While some Americans are exposed to market volatility by actively investing in stocks, others are affected by market swings through passive investing in mutual funds or allocations in their retirement accounts like 401(k)s and IRAs. When markets feel uncertain, clients may question whether their retirement plans carry the right level of risk — even when the market begins to recover.

What does recalibrating risk tolerance mean?

Recalibrating risk tolerance means reassessing how much market risk an investor is comfortable taking, especially during periods of volatility. Financial professionals may adjust asset allocation or incorporate annuity solutions to help balance growth potential with downside protection.

Why market volatility can change risk tolerance

It’s one thing to think hypothetically about saving and losing money. But watching actual retirement account balances tumble in market downturns can have real-world implications, like less income available throughout retirement. Those implications can be especially concerning for clients near retirement who don’t have time to recoup their losses.

Inflation and economic uncertainty are top drivers weakening consumer sentiment in the U.S.1 In fact, consumers are becoming noticeably more risk-averse2 as global risks, inflation and volatility concerns rise. If a client’s comfort level with risk changes, it could be the right time to talk about introducing more income protection into their retirement portfolio.

How financial professionals can start the conversation

One way to start the conversation is by asking your clients how the volatile market conditions have made them feel. Were they anxious, scared or unbothered by it? Are they inclined to change how their retirement savings are allocated, or are they content to let things stand?

Strategies for rebalancing retirement risk

Some clients, especially those in or nearing retirement, may want to dial back portfolio risk. In those cases, two recalibration strategies worth considering include:

- Directing more of their portfolio to fixed-income options

- Allocating a portion of their portfolio to annuities

Reducing market exposure to help protect savings and securing guaranteed income for retirement may help these clients feel more confident about staying on track toward their goals.

You may find some clients aren’t sure if their appetite for financial risk is the same or if it’s changed since you last talked about it. If they aren’t sure, Athene has developed an article and quick quiz you can share to help gauge how they feel now.

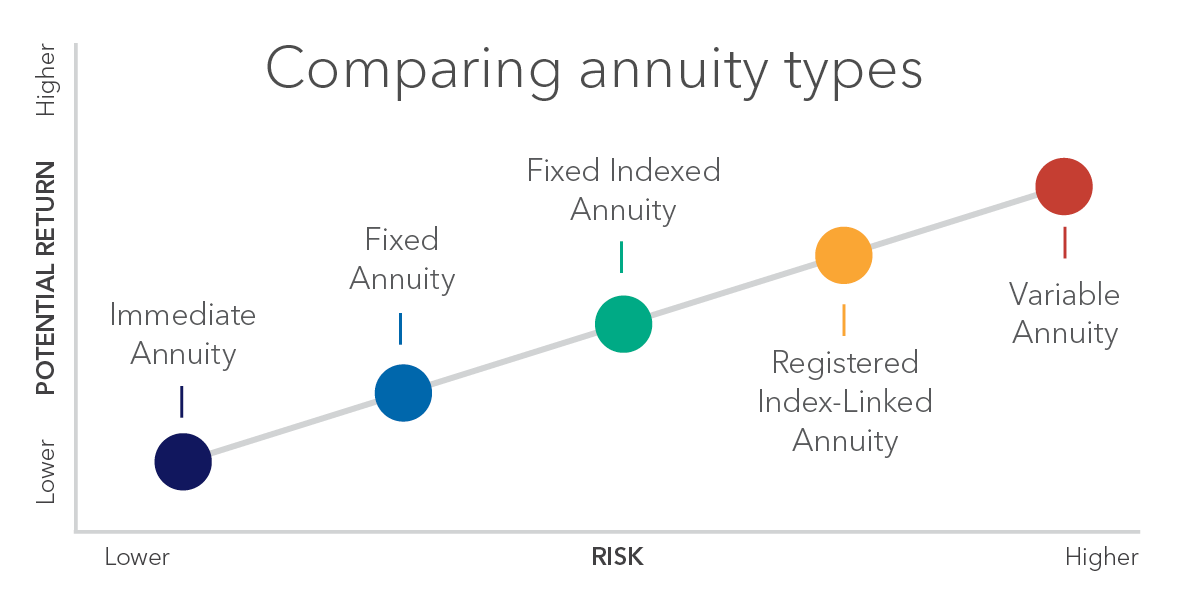

Understanding the annuity risk spectrum

Annuities, which convert money into future income, could be a solution to help your clients stay in their financial comfort zone.

With a variety of annuities available that align with different levels of risk, it’s becoming easier to include them in more retirement strategies to help meet clients’ growth, protection and income goals. You can use the annuity spectrum as a good visual to show clients how each type of annuity relates in terms of potential returns and level of risk.

For more conservative clients, immediate and fixed annuities may offer lower risk, but also lower potential returns. As the options move along the spectrum, potential for growth increases, but also with a higher level of risk. Fixed indexed annuities fall in the middle of the spectrum. Clients who want growth potential with protection from market downturns may find this annuity type to be the right match. For clients with a higher tolerance for risk, registered indexed-linked annuities may offer the potential for higher returns in exchange for reduced downside protection. At the top end of the spectrum, variable annuities carry the highest potential return and the highest level of risk.

Immediate Annuities

These carry the lowest risk. With an immediate annuity, your clients’ premium payment is converted to a guaranteed income stream for life, or for a specific period.

Fixed Annuities

This deferred annuity offers a fixed interest rate that’s guaranteed for a certain time. The guarantee may appeal to savers willing to sacrifice the potential for higher returns when the markets rise for the certainty of a fixed rate that won’t change with market fluctuations.

Fixed Indexed Annuities (FIAs)

FIAs have become increasingly popular with people who have a moderate appetite for risk. With these annuities, your clients can earn interest credits based in part on the upward movement of a stock market index while enjoying downside protection. If the net change over a given crediting period is negative, the client earns 0% in interest credits for that period, but never less than 0%. On the other hand, earnings are locked in so they can’t be lost.

Registered Index-Linked Annuities (RILAs)

RILAs are designed for people willing to accept more risk in exchange for the potential of higher returns. There’s also potential to earn interest credits tied to the performance of an underlying index or indices while providing a level of protection from market loss.

Variable Annuities

These annuities carry the highest level of risk because a client’s money is invested directly in the market. Variable annuities offer the highest growth potential on the annuity spectrum, but they also fully expose a client to market loss.

Risk-managed growth potential is the power behind RILAs.

Compare rates from many of the top carriers and see for yourself.

Helping clients align retirement plans with their comfort zone

Factors like policy changes, global events and market uncertainty can put traditional 60/40 portfolios under pressure. They can also leave financial professionals feeling conflicted while finding alternatives to help rebalance client portfolios as wealth transfers from one generation to the next.

The risks are real, but they’re likely not permanent. Depending on their comfort level with risk and progress toward financial goals, it may be time to reassess your clients’ retirement plans. Reallocating a portion of their savings to annuities could help better protect it against future volatility and offer growth potential without compromising their risk tolerance.

Frequently asked questions about risk tolerance in retirement

What is risk tolerance in retirement planning?

Risk tolerance refers to how much market volatility or potential loss an investor is comfortable accepting while pursuing long-term retirement goals.

How can annuities help manage retirement risk?

Certain annuities provide guaranteed income or principal protection, which may help reduce exposure to market volatility while supporting retirement income goals.

When should investors reassess risk tolerance?

Major market events, life changes or approaching retirement are common times to revisit portfolio risk levels.

Insights on Athene Connect. Tips, tools and resources to grow your business by helping clients retire with confidence.

1 Source: University of Michigan, Surveys of Consumers. March 2026; Federal Reserve Bank of New York. Survey of Consumer Expectations. 2026.

2 Source: Bloomberg. “Risk aversion has been Increasing Dramatically.” March 20, 2026.

Guarantees provided by annuities are subject to the financial strength and claims paying ability of the issuing insurance company.

Fixed indexed and registered index-linked annuities are not stock market investments and do not directly participate in any stock or equity investments. Market indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an index nor any market-indexed annuity is comparable to a direct investment in the equity markets.

Although fixed indexed annuities offer principal protection from market downturns, the deduction of applicable charges could exceed any interest credited, resulting in the loss of principal.

Registered index-linked annuities can only be marketed and sold by securities licensed financial professionals. They have a risk of substantial loss of principal and related earnings. They are designed to be long-term investment products used to help provide income for retirement and are not appropriate as short-term investments.