Read Time:

4-minute

article

7 client conversation tactics you’ll want to know

This content is categorized as:

Have you ever been told to cut down your sugar or caffeine intake? What about reducing stress? Although the health benefits are easy to understand, it’s not always easy for people to do what may be in their best interest. The same can be true with money matters. For example, why do some people hesitate buying an annuity when there are different types designed for growth potential, protection from market decreases or income?

Our partners at the UCLA Anderson School of Management have analyzed consumer behavior to help us understand. Incorporating their insights into retirement planning conversations could help you build stronger connections with your clients and help them feel more confident making financial decisions.

|

Tips for retirement planning conversations with clients

Discover ideas for talking with your clients about life expectancy (and why) plus other tips for breaking down common conversation barriers.

Get conversation guide

|

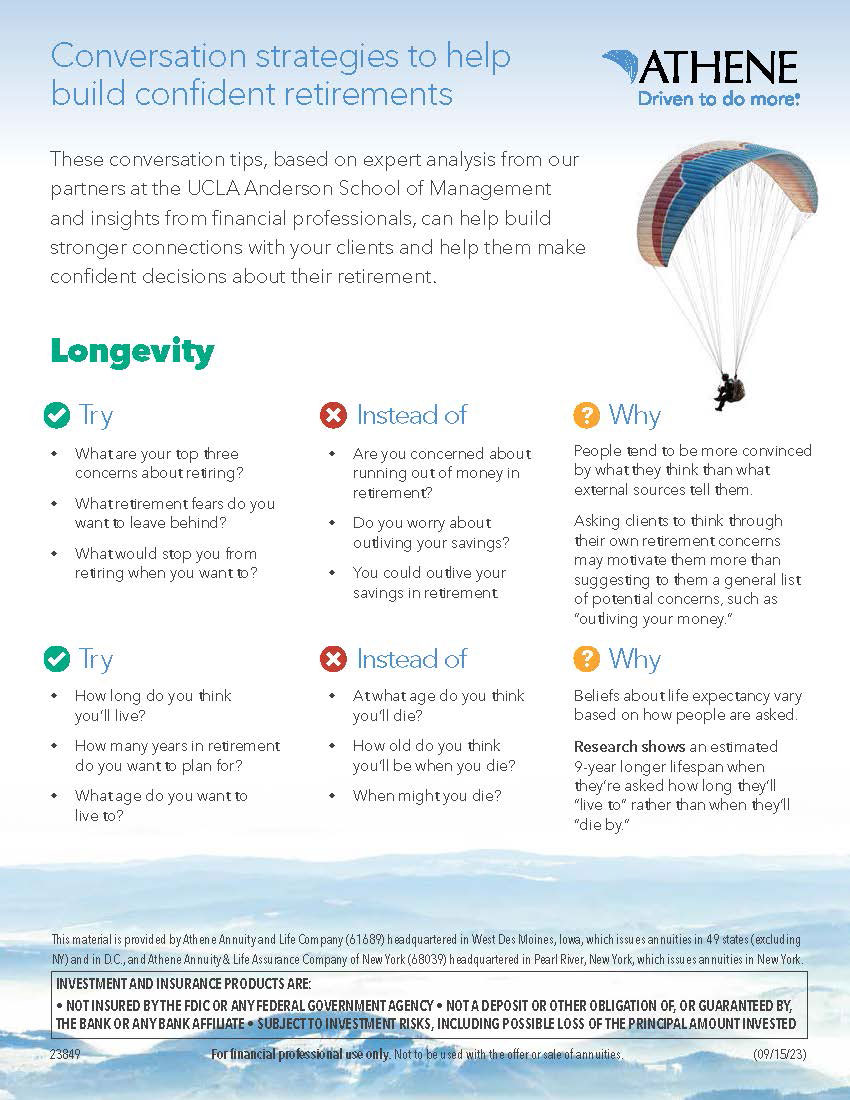

Managing client uncertainties

Running out of money in retirement is one of the most common concerns for people. While it may be tempting to share a list of potential concerns for clients to consider, ask clients to first think through their retirement concerns for a more meaningful outcome.

Conversation tip

Try: What are your top three retirement concerns?

Instead of: You could outlive your retirement savings.

Ease into client conversations, building rapport and listening before making suggestions that align with their needs. If a client doesn’t express a common concern, such as potentially outliving their money, you can ask probing questions to help uncover their principal concerns about retirement.

Fostering trust for hard conversations

Are you as comfortable talking with clients about life (and death) as you are talking about financial solutions available to help them achieve their goals? Some products, such as annuities, can lead to harder discussions like life expectancy. The trust built between you and a client may influence the trajectory these conversations take.

Discussions about life expectancy in relation to annuities could take a few different directions. They may stall out with clients who avoid talking about mortality, or it could lead to their concerns about passing away before getting to enjoy the deferred annuity value. Perhaps a friend or family member voiced the same concern, or a client may have recently lost someone close. Being sensitive to their body language, verbal cues and what’s happening in their lives can help you address concerns and keep the conversation alive.

Conversation tip

- Try talking about what happens to a client’s money after they’re gone instead of focusing on “lost money.”

- Try buffering a client’s negative feelings with positive ones.

- Read your clients for clues about how to diffuse negative emotions

(i.e., with empathy, humor, personal story, etc.)

How longevity questions are posed can also impact the direction an annuity conversation takes. For example, when questions about life expectancy are framed in terms of living rather than dying, people tend to estimate longer lifespans, according to the Journal of Risk and Uncertainty.

Conversation tip

Try: How long do you think you’ll live?

Instead of: At what age do you think you’ll die?

It can be difficult to know how someone will react to conversations involving their mortality until it comes up. But avoiding the topic may be the difference between a client feeling financially confident about retirement or not.

Understanding annuities: Illusion or reality?

The word “annuity” may also cause concern because of faulty assumptions, misinformation or having a limited idea about how annuities work. On the other hand, some people believe they understand more about annuities than they do.

With retirement planning, accurate perceptions and clear communication could impact a client’s future financial security. But there are some communication strategies to help get past potential objections.

First and foremost, let client needs drive the conversation. If some clients are concerned about losing money in volatile market conditions, for example, talking about how a fixed indexed annuity can guarantee they won’t lose money in a down market may help alleviate anxiety. If other clients are concerned about outliving their money or losing access to it, talking about a fixed annuity’s guaranteed income stream or free withdrawal period could help set their minds at ease.

Conversation tip

Try: Access some of your money when you need it.

Instead of: The annuity’s liquidity rider provides access to a portion of your funds.

Estimating future spending

Knowing how much money clients may need in retirement may pose another challenge. When clients imagine themselves 20 years from now, can they see a clear picture of themselves? It can be harder to paint a clear mental picture of the distant future, which is why it’s easy to underestimate how much money it can take to retire. Having your clients think specifically about their current expenses can help them estimate future spending more accurately.

Conversation tip

Try: What would your monthly expenses be if you retired next month?

Instead of: How much money do you think you’ll need in retirement?

The stronger your client connections are, the more you can understand about their needs, concerns and motivations. That level of insight can position you as their trusted retirement planning resource and help you grow your business.

Find more insightful tips in ourconversation guide

Insights on Athene Connect. Tips, tools and resources to help grow your business by helping clients retire with confidence.